|

|

| |

|

|

| |

| |||||||||||||||||||||||||||

|

|

Budget Scramble

Social Security, Medicare Surpluses Are Key Prize

as Federal Ledger Returns to Red

A year ago political leaders of all persuasions, including President Bush, vowed that the Social Security surplus would be used only to pay benefits or to reduce the national debt. Today the so-called lockbox that was supposed to protect this surplus lies shattered. As red ink has once again begun to flow over the federal budget, part of the trust fund reserves has already been borrowed for other purposes. And budget officials expect borrowing to continue for at least eight more years.

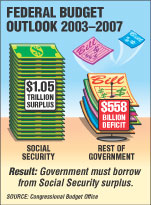

The turnaround has set off a budget scramble in which the Social Security and Medicare surpluses—now at $1.3 trillion and the only surpluses left—are the key prize. And how this money is used, and what the impact will be, have become major concerns for many Americans. The Social Security surplus results from the trust fund taking in more in payroll taxes than it pays out in benefits—a deliberate buildup to help prepare for the coming upsurge of baby-boomer retirements. "The first thing people should be clear about is that this borrowing does not affect Social Security's ability to pay benefits," says John Rother, AARP director of policy. "The trust fund is intact and still collecting interest on its Treasury bonds." The main effect of continued borrowing, he says, will be on the economy. If the trust fund surplus is not used to reduce the national debt, as it was for four recent years, that debt will not be paid off and interest payments will be higher.

Rother says it is AARP's position that as trust funds continue to be tapped, this money should be used as it was intended. "The Social Security and Medicare trust funds were created to ensure the health and retirement security of our aging population," he says, "and their surpluses should be used for Social Security and Medicare before anything else." Others think differently. Bush, in his 2003 budget, proposes big increases in defense and national security spending—increases that, for the most part, Congress is likely to approve. But while he earmarks $190 billion over the next decade for a prescription drug program, the president would also make last year's tax cuts permanent and add new tax cuts—a move many oppose. WHY THE RED INK?

Borrowing from the trust fund resumed last year, when $33 billion was diverted to other uses. This year $152 billion more is expected to be borrowed, and the CBO sees the trend continuing each year through 2009. DEFICITS: A PROBLEM OR

NOT? The multitrillion-dollar question therefore is, How long will deficits last? Bush says that if Congress follows his plan, balance could be restored to the overall (or "unified") budget in 2005. His approach involves making significant cuts in certain programs and borrowing from the Social Security surplus. But others, like Sen. Kent Conrad, D-N.D., chairman of the Senate Budget Committee, believe the president paints too rosy a picture. "We now face a decade of red ink," Conrad said at a recent hearing. And "the biggest reason," he continued, "is because of the tax cut." Economists say two factors will largely determine whether or not deficits become a serious problem: how fast the nation recovers from recession and whether government spending is kept at reasonable levels. Like most economists, Robert D. Reischauer, president of the Urban Institute, a Washington think tank, believes the recession may be behind us but that recovery may be slow. He's concerned, however, that "it's going to be real difficult to impose fiscal discipline" on Congress.

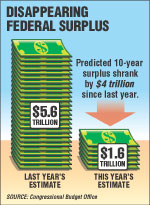

Larry Sabato, a political scientist at the University of Virginia, shares that concern. "Once you go into deficit," he says, "the restraints are gone for all practical purposes." He believes this will especially be the case as the parties jockey for public favor before the November elections. WHAT LIES AHEAD Daniel Mitchell, a senior fellow at the Heritage Foundation, a conservative Washington think tank, backs most of the president's proposal. He says speeding up the tax cuts is necessary to boost the economy. "A tax cut delayed," he says, "is an economic benefit deferred." Richard Kogan, a senior fellow at the Center on Budget and Policy Priorities, takes an opposite tack. "Seventy-one percent of the tax cut," he says, "went for people in the top one-fifth of the income spectrum." As a result, he favors "not locking into place portions of the tax cut that haven't yet occurred." Although the tax debates are expected to raise political tempers on Capitol Hill, most experts believe that neither a speeding up nor slowing down of the tax cuts will take place. Reischauer says the nation is coming off several years of surplus and is therefore much better off than it was when deficits soared in the 1980s and early 1990s. "Compared to our expectations [of huge surpluses] of a year or two ago the situation has deteriorated significantly," he says. "But we shouldn't pretend it's worse than in fact it is." Congress can still control the situation. "If we slip back into serious budget difficulties," Reischauer says, "it will be because of decisions yet to be made." Still, the University of Virginia's Sabato adds a note of caution. "People should be concerned about the budget situation," he says, "because if you look back on the history of budget deficits, they tend to build on one another."

|

||||||||||||||||||||||||||

"The easy [budget] areas on which to impose discipline have been

used up," he says, and divided government and the narrow balance of

political power "create pressures to spend more and cut taxes more."

"The easy [budget] areas on which to impose discipline have been

used up," he says, and divided government and the narrow balance of

political power "create pressures to spend more and cut taxes more."